United Kingdom

United Kingdom

After a significant rise in both conventional and index-linked gilt yields, we are working with our clients to review collateral sufficiency and leverage in their liability hedging strategies. In the new interest rate and volatility environment, we think it makes sense for clients to ensure collateral pools continue to support their liability hedges.

We encourage our clients to review the plans they have in place and their associated governance/decision-making frameworks in light of these developments. It is critical that collateral top-ups can be made efficiently, as higher volatility may lead to increasing collateral requirements at short notice.

For many, we believe that it might be best to top-up collateral pools sooner. This could help reduce the risk of being a forced seller of assets at potentially inopportune times and simplify governance. Other techniques such as ‘waterfalls’ and synthetic equity strategies could further increase the resilience of portfolios whilst ensuring investment efficiency is maintained.

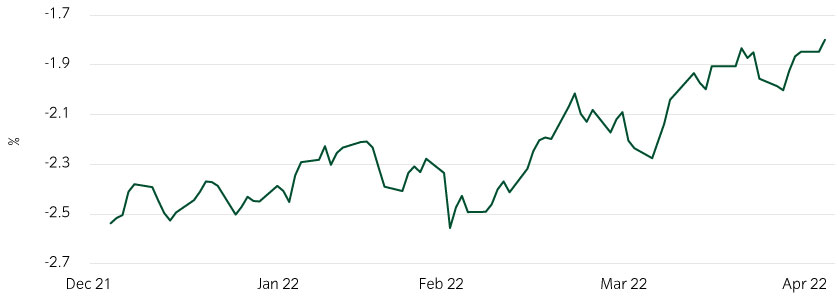

Figure 1: 20-year gilt yields soared in 20221

Market moves and the impact on funding levels

There was a 0.94% rise in 20-year conventional gilt yields and a 0.71% rise in index-linked yields from 31 December 2021 to 30 April 2022. This rise is among the fastest and most substantial since many LDI mandates were established. In our experience, existing collateral pools have served our clients’ needs well to date and most of our clients have benefitted from the yield rises – to the extent they are not fully hedged.

The associated reduction in bond values has led to higher leverage in hedging mandates, and in some cases, this requires attention. For example, a scheme that started the year with a 3x levered liability hedge would have been a net beneficiary of the moves in gilt markets but, notwithstanding that, may have seen the leverage of its liability hedging portfolio increase to 4.5x.

Figure 2: 20-year index-linked gilt yields also rose in 20222

Strategy implications

Over the longer term, the leverage used in liability hedging strategies has substantially benefitted pension schemes. It has helped them achieve their intended goals of both hedging large amounts of risk and maintaining exposure to growth assets to meet return targets. In aggregate, this has materially helped keep pension provision affordable.

To date, the improved funding position has allowed many clients to raise cash through the sale of growth assets, in order to increase the size of the collateral pool backing leveraged positions and so repair the hedge’s resilience to future changes in yields.

Having said this, making sales of assets as and when needed to top-up collateral pools is not the only way to deal with collateral uncertainty. For example, some pension schemes may benefit from reviewing the collateral waterfall frameworks they have in place, for example considering:

- the composition of the assets used,

- the anticipated liquidity and disinvestment timeframes,

- the levels at which sales and purchases are made, and

- the amount of discretion given to their investment manager.

Additionally, replacing physical equity holdings with equity exposures through derivatives could enhance efficiency and resilience.

Along with economic benefits, these steps may give greater peace of mind and reduce the future governance burden on trustees.

Please let your usual Insight contact know if you would like more information about your portfolio’s resilience.

Also to keep abreast of daily market moves, please visit our Market Monitor which we update every weekday morning with levels at the end of the previous working day.