United States

United States

Reversal of fortune?

As the pandemic hit, US Treasury yields were driven to fresh all-time lows, the yield curve flattened, money market funds swelled, and credit issuance was a record-shattering ~$2trn1 in 2020.

Credit markets still rallied given extraordinary central bank support and retail buying. But these factors created some technical headwinds among many traditional investors:

- Overseas investors saw a dwindling premium, particularly given hedging costs.

- Pension plans became hesitant about increasing their interest rate hedge ratios (although, see our Liability Driven Insights arguing the case for higher hedge ratios given lower yields).

- Insurance investor AUM grew slower than credit market issuance, making it harder for insurance company demand to help absorb the new supply.

However, as the economy continues to recover, the yield curve has steepened and so the technical tide could be about to turn.

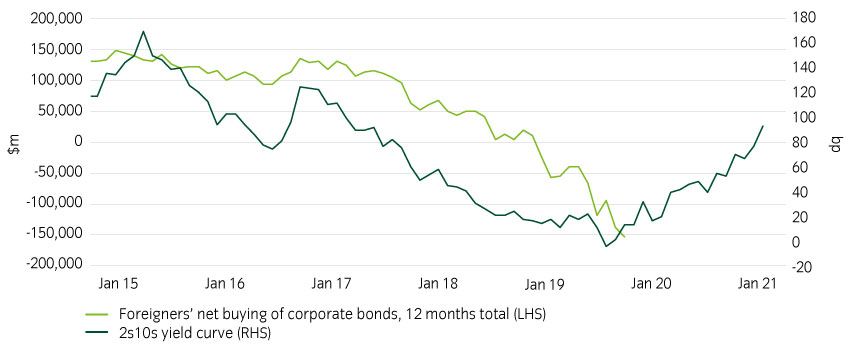

A steepening curve attracts foreign buyers

International US credit demand tends to correlate with the shape of the US Treasury yield curve, subject to a 1-year lag (Figure 1).

Figure 1: Foreign US credit buying is yield curve sensitive2

A flattening curve in 2019 resulted in less foreign demand in 2020. However, for much of 2020 and indeed the last two months, the curve has been re-steepening.

While the Fed’s extraordinary policy has kept front-end yields anchored, long-end yields have been rising – given a light at the end of the pandemic increasingly visible and the prospect of rising Treasury supply to finance the Biden administration’s fiscal stimulus ambitions. This dynamic has led to steepening of the US treasury curve from 60bps to nearly 200bp3.

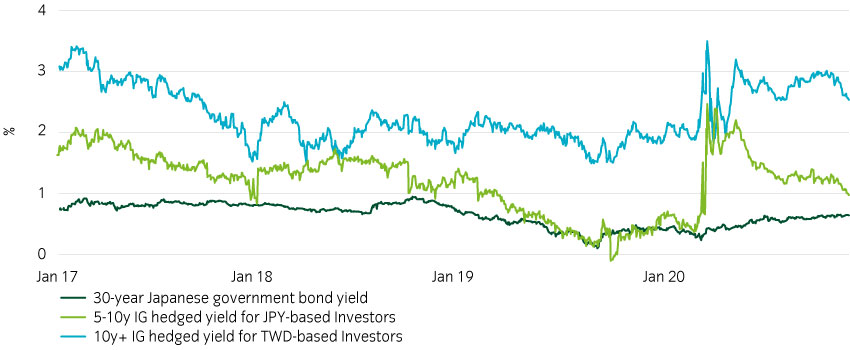

A steeper US curve tends to attract, in particular, Japanese pension funds and Taiwanese life insurers into longer-dated US credit, with the aim of locking in income and ‘rolling down’ the curve4.

Hedging conditions have also improved for overseas institutions. Hedge-adjusted US credit yields are near three-year highs for Taiwanese investors (Figure 2).

Figure 2: Taiwanese hedge-adjusted US credit yields are around 3-year highs5.

In Europe, core government bond yields are still in negative territory. US credit can offer Europeans a potential ~80bp6yield gain on US credit after hedging (Figure 3).

Figure 3: Hedging costs for European investors are relatively low7.

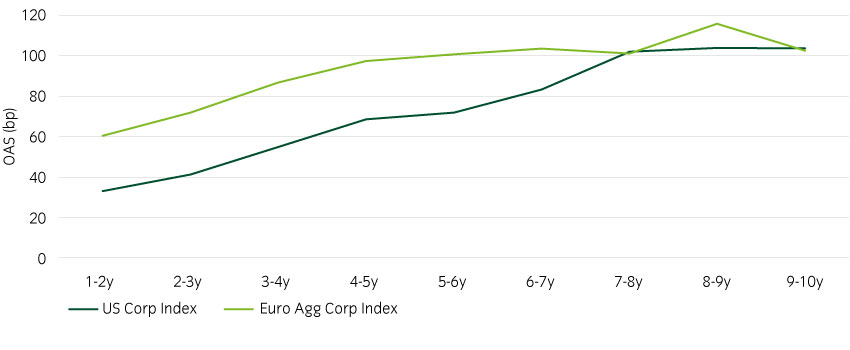

Credit curves are also notably steeper in the US than in European counterparts, given greater long-dated issuance (Figure 4).

Figure 4: US credit curves are steeper than Europe8.

Foreign demand has already materialized in 2021 and is being met with long-dated issuance.

For example, 7-Eleven9 raised $10.95bn at the end of January to help fund its acquisition of Marathon Petroleum Corp.’s gas-station business. It started offering the bonds during Asia hours. There were $17bn of orders placed before the New York open. Elsewhere, Morgan Stanley10 sold the first 31-year non-hybrid financial debt tranche of the year in January.

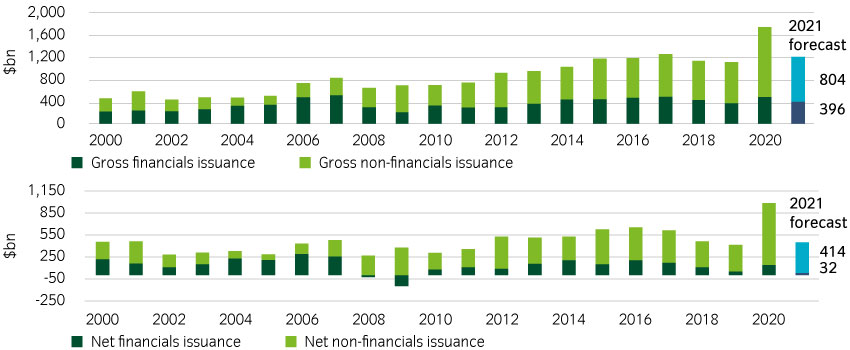

New supply in 2021 is set to fall sharply

Investment grade (IG) supply in 2020 was the highest on record at ~2trn, and a ~50% increase over 2019. However, it increasingly looks like a one-off.

Expectations are for gross issuance to fall ~30% in 2021 and net issuance to fall ~55% (Figure 5), especially as corporates use outsized cash balances to buy back existing debt.

Figure 5: Gross and net issuance is forecast to fall sharply in 202111.

Since the start of October, net issuance has been -$3bn. Year-to-date in 2021, net supply has been down 49% compared to the previous year12.

The 2020 deluge was largely a result of corporates raising defensive liquidity pools to ride out the pandemic-related uncertainty while also locking in even lower yields for longer. Most of this activity is done and dusted, particularly among the largest IG names, which are now largely flush with cash.

For 2021, this leaves the IG market with refinancing needs of only ~$1trn (including only $40bn in the tech sector – often a source of massive deals) . Otherwise, M&A financing will potentially be the sole main driver of further supply this year13.

Plenty of cash remains on the sidelines

Following the liquidity crisis of March 2020, there was a rush to the safety of money market funds. Surprisingly, even as markets rallied sharply, this trend has only reversed slightly (Figure 6).

Figure 6: Assets in money market funds12.

This indicates that investors are potentially under-invested on the whole. Absent further economic shocks, investors may increasingly start putting cash to work. High quality investment grade credit may be a natural destination.

Playing 2021's technical tailwinds: BBBs offer the potential sweetspot

Issuance is potentially likely to be particularly low in the BBB segment in 2021. This is because BBB companies have the least capacity to engage in leverage-inducing M&A. Many are in fact de-leveraging following their own recent M&A transactions.

Large BBB names also tend to be the primary investment destination of Asian institutions, given generous capital treatment. We also expect Asian capital to invest beyond 7-year maturities. We also see value further out the curve, such as 20 to 30-year segment which is also relatively steep.

US dollar emerging market (EM) corporate debt also currently screens cheap to us versus US corporates and we believe it is potentially an attractive investment for investors with cash on the sidelines. The asset class proved itself resilient in 2020, given a corporate deleveraging trend, with many names actively issuing to mitigate refinancing risks. Default rates ended the year with relatively healthy 3.5% default rates (roughly half the rate of US high yield). EM corporate debt offers also higher yields with lower duration (for example, the CEMBI: corporate benchmark only has a duration of 5), which can help insulate investors from the risk of a rising rate environment. Lastly, the pandemic showed how divergent economic outcomes can be and an EM allocation, including Asia, can add geographical diversity, which has been able to normalize economic activity faster than the West.

As ever — be selective

We believe that security selection within these medium and longer-dated BBB corporates will be key. The pandemic and changing policy environment have heavily bifurcated the market between ‘winner’ and ‘loser’ sectors.

We look for selective opportunities down the ratings spectrum within ‘winners’ and best-in-class credits within the ‘losers (see Credit Insights: Playing Election Winners and Losers for more).

The technical headwinds of 2020 may not have prevented a sharp tightening of credit valuations following the height of the crisis. However, in our view, there remains significant opportunity in targeting the potential beneficiary of 2021’s technical tailwinds.