MARKET REVIEW

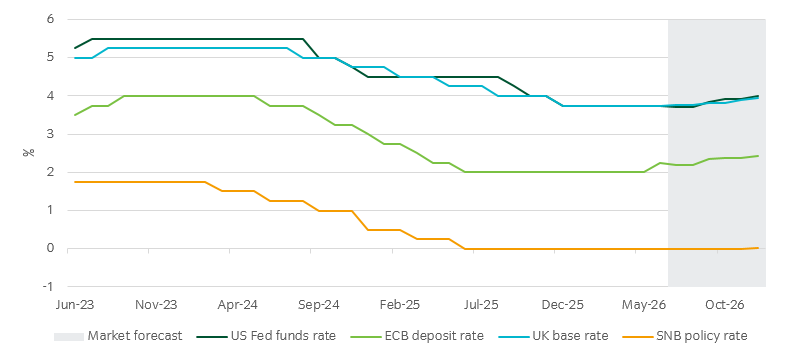

European Central Bank (ECB): The ECB Governing Council voted to raise its key deposit rate to 2.25% in June, the first hike since 2023 and in line with expectations. ECB President Christine Lagarde emphasised that the war-driven surge in energy prices is generating renewed inflation pressures, while reiterating that policy will remain data dependent, stating that decisions will be based on “our assessment of the inflation outlook and the risks surrounding it”, rather than following a pre-set rate path. Meanwhile, Eurostat reported that the annual Harmonised Index of Consumer Prices (HICP) inflation rate rose to 3.2% in May, up from 3.0% in April and in line with expectations. GDP data showed the euro-area economy shrank by -0.2% quarter-on-quarter in the first quarter, revised downwards from the initially reported 0.1% rise. The ZEW Economic Sentiment Indicator recovered substantially to +9.5 in June, up from -9.1 in May and well above expectations of -7.2. Likewise, consumer confidence rose slightly to -17.7, up from May’s -19.

Swiss National Bank (SNB): The SNB left its policy rate unchanged at 0% at its June monetary policy assessment and reiterated its willingness to intervene in foreign-exchange markets if necessary to counter excessive appreciation of the Swiss franc. Manufacturing activity remained resilient during the second quarter, with the procure.ch Purchasing Managers' Index (PMI) easing to 54.3 in June from a near four-year high of 57.3 in May but remaining comfortably above the 50 threshold that separates expansion from contraction. The KOF Economic Barometer improved over the period, pointing to a gradual strengthening in economic momentum, although it remained below levels typically associated with robust growth. Inflation remained low by international standards but increased to 0.8% year-on-year in June from 0.6% in May, driven largely by energy-related effects, while underlying price pressures remained contained and consistent with price stability. Consumer confidence remained subdued, reflecting continued caution among households despite signs of improvement elsewhere in the economy. Meanwhile, Swiss GDP expanded solidly in Q1. Looking ahead, the SNB expects growth to moderate somewhat as weaker global conditions weigh on activity, while continuing to forecast GDP growth of around 1% in 2026 and around 1.5% in 2027.

UK Bank of England (BoE): At its June meeting, the BoE Monetary Policy Committee voted 7-2 to maintain the bank rate at 3.75%. Annual headline CPI inflation remained at 2.8% in May, beneath expectations of 3.0%. Meanwhile, the core rate, which removes the effect of more volatile items such as food and energy, edged up slightly, by came in below expectations at 2.6%. The Office for National Statistics reported UK unemployment fell to 4.9% in the three months to April, down from March’s 5%. Meanwhile, average earnings growth rose to 4.4% year-on-year (including bonuses) for the three months to April 2026, in line with the previous period’s 4.4% and above expectations of 4%. The GfK Consumer Confidence Barometer remained at -23 in June. Likewise, month-on-month retail sales volumes rose by 1.2% in May, down from April’s downwardly revised fall of 1% and ahead of expectations.

US Federal Reserve (Fed): The Federal Open Market Committee unanimously voted to leave the federal funds rate target range unchanged at 3.5%-3.75%. Policymakers noted that “Economic activity is expanding at a solid pace despite elevated uncertainty”. The “dot plot” which shows members policy expectations also signalled a clear shift, with a majority of officials now projecting rate hikes this year, reversing the more dovish outlook seen only a few months ago. Speaking after the meeting, new Federal Reserve Chair Kevin Warsh offered little guidance on inflation, focusing instead on plans to reform the central bank. Annual Personal Consumption Expenditures (PCE) inflation, the Fed’s preferred measure, rose to 4.1% in May, in line with expectations, while core PCE inflation increased to 3.4%, marginally above expectations. Annual Consumer Price Index (CPI) inflation rose to 4.2% in May, up from April’s 3.8% and in line with expectations. Activity data were also firmer, with the Institute for Supply Management (ISM) Manufacturing PMI rising to 54.0, from April’s 52.7 and above expectations of 53.0, while the ISM Services PMI increased to 54.5, from 53.6 and above forecasts of 53.8. Annualised first quarter GDP growth was confirmed at 2.1%, up from the previous estimate’s 1.6% and above the 0.5% rate of the final quarter of 2025, reflecting higher than forecast business investment in equipment. In employment data, non-farm payrolls indicated that the US economy added 172,000 jobs in May, well above expectations of 85,000, but slightly down from April’s upwardly revised 179,000. Consumer confidence improved over the month, with the University of Michigan Consumer Sentiment Index rising to 49.5, likely reflecting the end of the Middle East conflict.

Figure 1: Central bank rates history and future market pricing1