The outlook for global growth became more pessimistic early in the second quarter, but has recently rebounded and should further improve, albeit moderately, driven by the decline in oil prices.

We are long-term bearish on the USD, but over the quarter we think there is room for the USD to appreciate driven by both a return of US exceptionalism, a more hawkish position at the Federal Reserve, and higher US real rates. We expect perceptions of US exceptionalism to gradually ease as lower oil prices support growth in energy importing countries, including Europe.

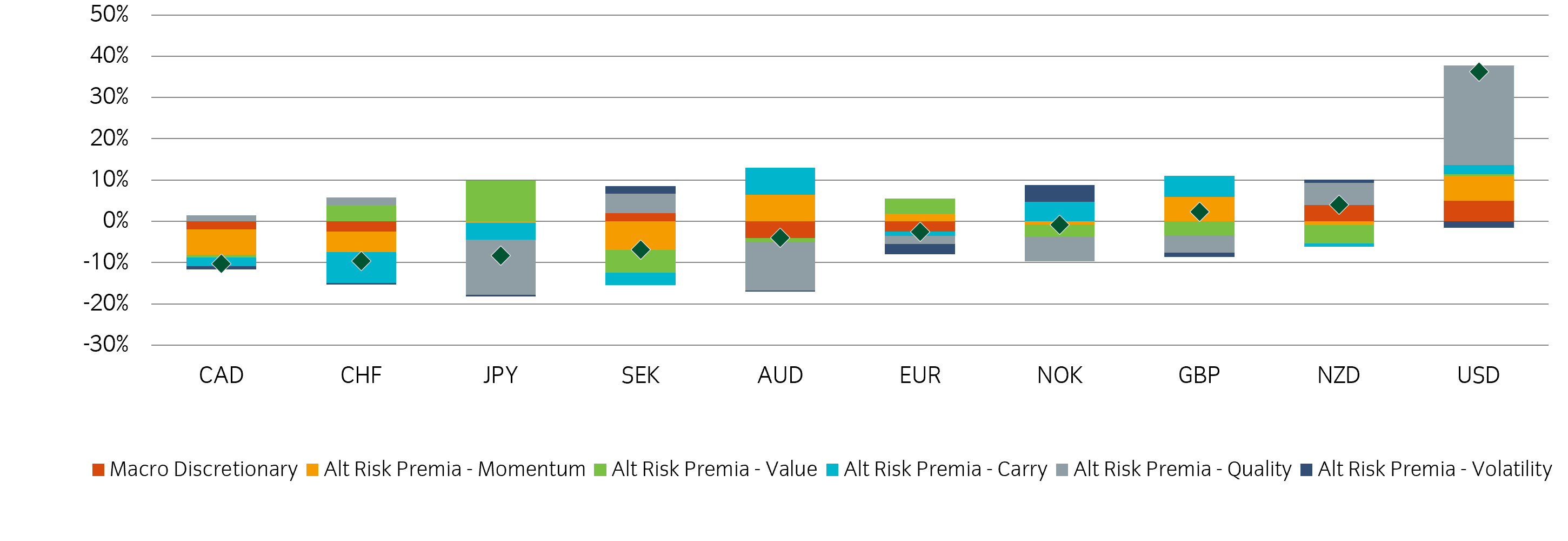

Our Alt Risk Premia model holds a long USD exposure driven by the Quality and Value Factors – Momentum and Volatility are only partially offsetting the positive USD exposure. Elsewhere, we favour longs in AUD and EUR versus shorts in CAD, JPY and SEK. Macro Discretionary tactically long USD vs low yielding currencies.

The alpha view

Given the uncertainty around the policy outlook our Macro Discretionary exposure is limited. We have a modest USD long, but the nature of the trade is tactical in nature, not strategic.

The Alt Risk Premia model also holds a long USD exposure driven by the Quality, Momentum, and Carry Factors.

Elsewhere, we favour shorts in CAD, CHF, JPY and SEK. The overall portfolio is shown in Figure 1.

Figure 1: Insight currency absolute return exposure

Source: Insight. Data as at 1 July 2026. Note: dark green dot shows aggregate position.

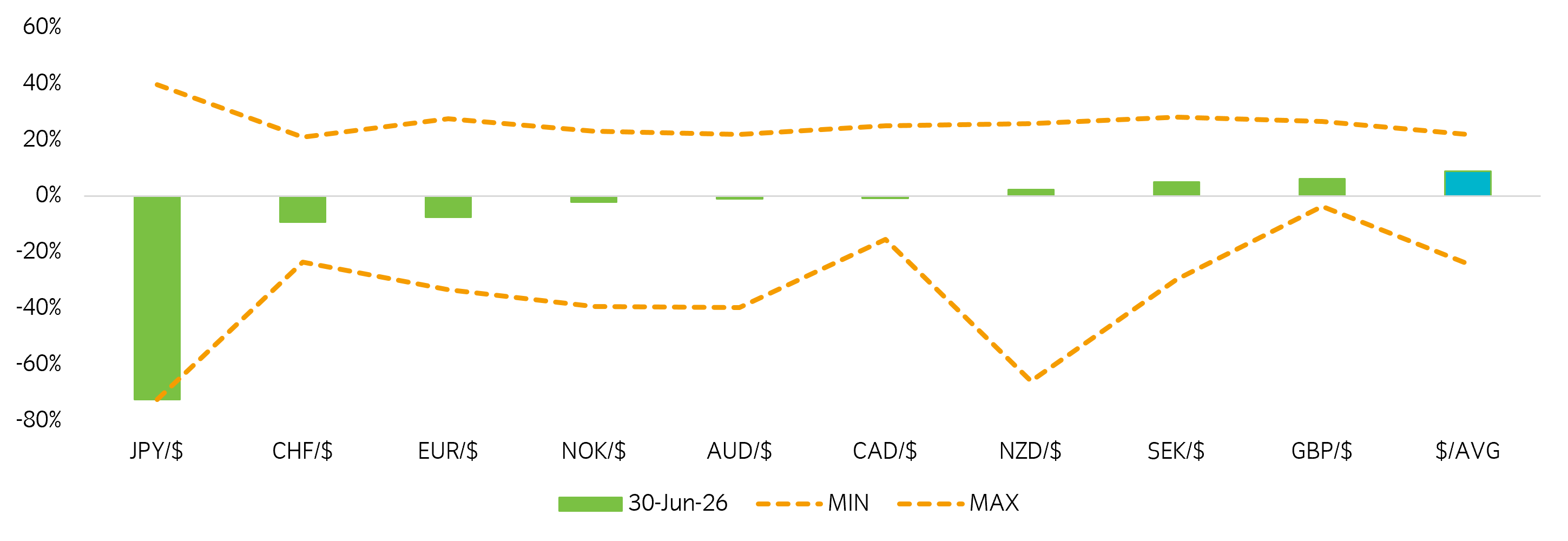

Longer-term valuation overview

For less agile longer-term investors whose investment decisions lean more heavily on valuation metrics, a few points can be made.

- The USD is moderately expensive.

- The CHF and EUR are moderately cheap, while JPY is very cheap.

- The AUD, CAD, NOK, and NZD look close to fair value.

- The SEK and GBP are slightly expensive.

Figure 2: Local currency overvaluation (+) and undervaluation (-) versus USD

Source: Insight. Data as at 1 July 2026.