Introduction – What are US municipal bonds?

U.S. municipal bonds are debt securities issued by states, cities, counties, and other governmental entities to fund public projects such as schools, highways, airports and water systems. These bonds offer investors a way to earn interest while supporting infrastructure and community development. Bonds issued by a state and funded via tax revenues are known as general obligation (GO) bonds, while bonds secured by the income stream of an infrastructure asset are known as revenue bonds.

US municipal bonds come in two primary forms:

- Tax-Exempt Bonds: Interest income is exempt from US federal income tax and often from state and local taxes. These are ideal for US-based investors in higher tax brackets.

- Taxable Bonds: Interest income is subject to taxation, making them more suitable for non-US investors, who do not benefit from US tax exemptions. These bonds often offer higher yields to compensate for the lack of tax benefits.

In our experience, for many investors outside the US, the municipal bond market remains an underappreciated asset class

Why consider US municipal bonds

Opportunities offered by a fragmented market:

The US municipal bond market comprises 61,000 issuers,1 approximately eight times the number of US corporates. In our view, this greater level of fragmentation presents significant opportunities for active managers to add value. However, capitalising on these opportunities demands rigorous credit analysis by a dedicated specialist team. In the case of revenue bonds, this entails a meticulous assessment of the unique risks and characteristics associated with the underlying infrastructure assets of each instrument.

Strong credit fundamentals

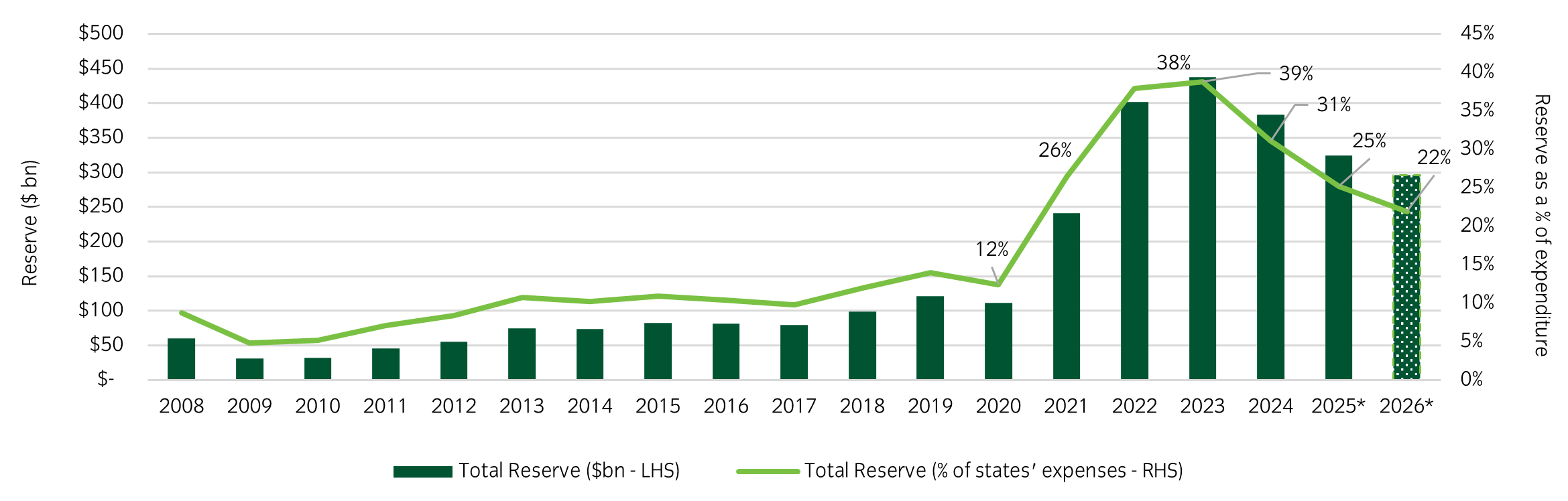

In aggregate, current municipal credit conditions are supportive for the asset class, bolstered by healthy state balance sheets and prudent management of cash reserves. For example, state total balances – combination of cash reserves that state governments set aside to help cover unexpected budget shortfalls or revenue declines and general fund ending balance – remain near the highest levels seen in decades, projected to reach $287bn in 2026 (see Figure 1). Likewise, the median level of state total cash balances remains well above pre-pandemic levels.

Figure 1: US states’ total balances remain near record high2

Likewise, municipal fundamentals are further bolstered by strong revenue collection, with most states reporting revenue collections exceeding budget projections. In cases where revenues fell short, reduced spending helped maintain budget surpluses, allowing states to build reserves and reduce debt. In addition, the aggregate revenues are expected to grow by 1.9% in fiscal year 2025 versus fiscal year 2024, highlighting the strength underlying the municipal bond market.3

Strong historical resilience and credit quality relative to US corporates

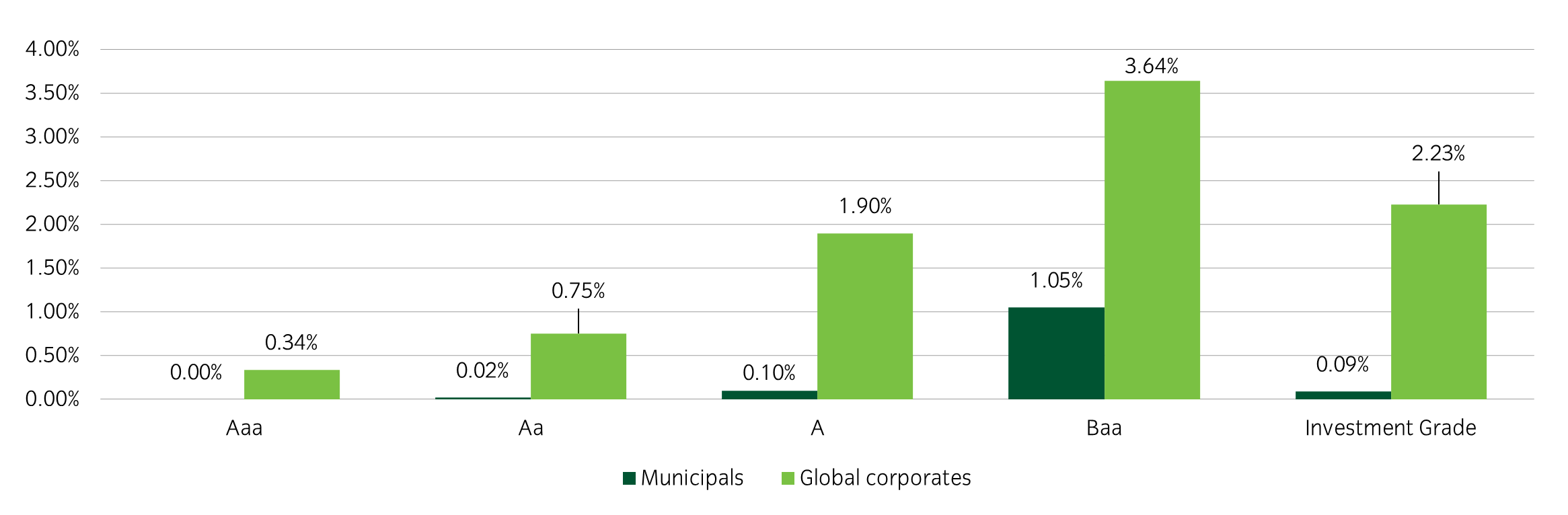

The quasi-public nature of municipal bonds has resulted in significantly lower historical default rates and higher recovery rates than global corporate bonds. For example, from 1970 to 2022, investment grade muni bonds, from AAA to BBB, experienced a cumulative default rate of only 0.09% versus 2.23% of IG global corporates within 10 years of issuance. The aggregate muni default rate is around one quarter of the average default rate for US AAA corporates of 0.34%.3

Munis also have displayed a lower default rate for any given credit rating (see Figure 2)

Figure 2: Historical defaults rates have been lower for munis4

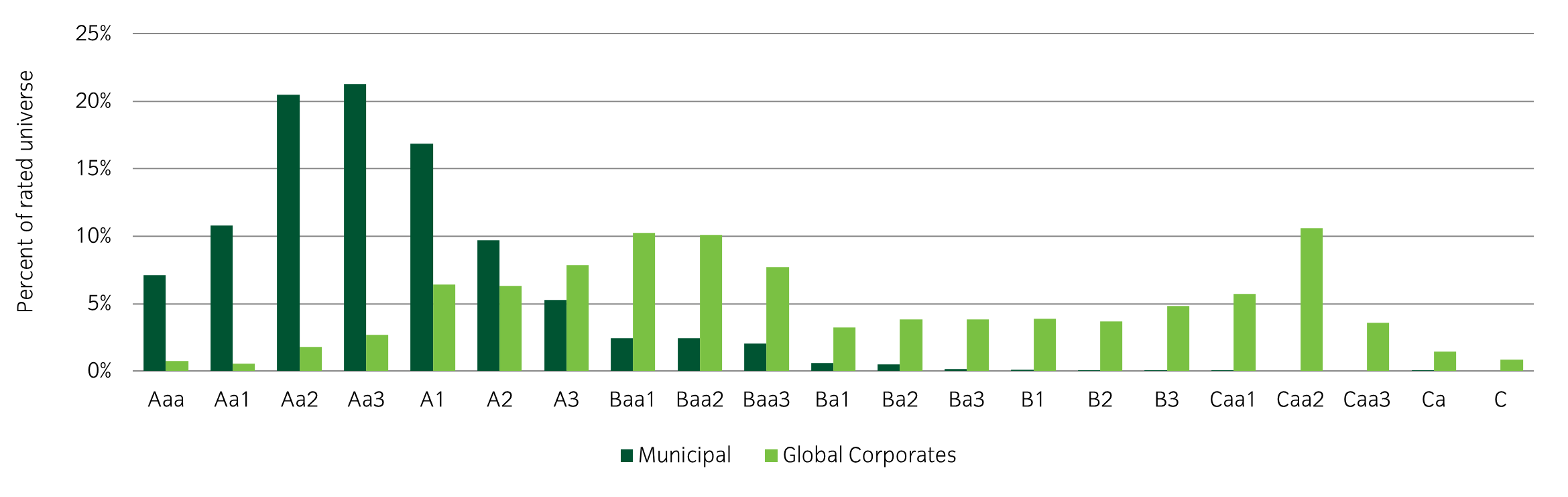

Likewise, the asset class has exhibited a historically higher aggregate credit quality than US corporates, with a much greater proportion of the universe boasting ratings of A3 and above (Figure 3).

Figure 3: US municipals versus global corporates rating distributions5

How can US municipal bonds complement fixed income portfolios

- Liability Matching: Long-dated maturities suitable for pension and insurance portfolios.

- Inflation Hedging: Some structures include inflation-linked features.

- Duration Management: Wide range of maturities and callable structures.

US municipal revenue bonds

In our view, municipal revenue bonds possess several advantages over general obligation bonds, such as strong credit fundamentals, greater insulation from political risk and historically attractive yields. We believe these characteristics, in combination with a focus on high-quality, stable issuers in economically strong services areas, represent bond income sources that are better insulated from economic slowdowns than tax-reliant general obligation (GO) bonds.

Why US municipal revenue bonds

Attractive yields: Taxable municipal revenue bonds often offer higher yields than comparable sovereign or corporate bonds.

Project-specific risk: Investors can assess risk based on the performance of the underlying asset (e.g., airport traffic, utility usage).

Currency diversification: Exposure to U.S. dollar-denominated assets can hedge against local currency volatility.

Strong legal framework: U.S. municipal bonds operate within a well-regulated and transparent legal environment.

Conclusion

For professional investors, we believe U.S. municipal bonds – especially taxable revenue bonds – offer a compelling opportunity to access high-quality, yield-enhancing assets. Their structural diversity, credit resilience, and alignment with infrastructure investment themes have the potential to make them a valuable addition to global portfolios.

Why Insight for munis

Having launched one of the first infrastructure US municipal bond strategies for overseas investors in 2017, the Municipal Bond Team at Insight Investment understands the varying needs of its global base of investors.

Highly experienced specialist munis team

Insight’s highly experienced investment and trading teams have operated through multiple market and business cycles, providing the ability to navigate the idiosyncrasies in the market to maximise the opportunity set and harness the unique attributes of revenue bonds.

Revenue bond focus

We believe revenue bonds possess several advantages over general obligation bonds, such as strong credit fundamentals, greater insulation from political risk, and historically attractive yields. We believe these characteristics, in combination with a focus on high-quality, stable issuers in economically strong services areas, represent bond income sources that are better insulated from economic slowdowns than tax-reliant general obligation bonds.

Exploiting opportunities in a fragmented market

The fragmented nature of municipal bonds and infrastructure projects financed, and a buyer base dominated by retail investors, provides a distinct opportunity to exploit market inefficiencies. Detailed credit analysis by a specialist team is required, in our view, to identify and assess the unique risks and characteristics of the underlying infrastructure assets and how they are being managed.

Most read

Fixed income

March 2026

Monthly fixed income review and outlook

Global macro, Fixed income

October 2023

Yield-curve inversion – an unreliable recession signal?

Global macro, Economics

May 2023

Why central banks may struggle to solve the inflation puzzle

Fixed income

April 2025