| "Positive correlation is most likely when inflation surprises to the upside, when supply-side shocks dominate, or when central banks are tightening into slowing growth." |  |

Why are equities and bonds usually negatively correlated?

Risk assets such as equities and credit typically respond differently to growth shocks than high-quality government bonds. In a risk-off or recessionary environment, equity prices are likely to fall as the earnings outlook deteriorates, while government bonds offer a safe haven, with the added hope that central banks ease policy, pushing yields lower and bond prices higher.

Why do equity-bond correlations become positive?

Positive correlation is most likely when inflation surprises to the upside, when supply-side shocks dominate, or when central banks are tightening into slowing growth. All three scenarios can lead to higher bond yields and create headwinds for corporates. In such environments, bond and equity prices can both come under pressure, a scenario we have witnessed repeatedly in recent years.

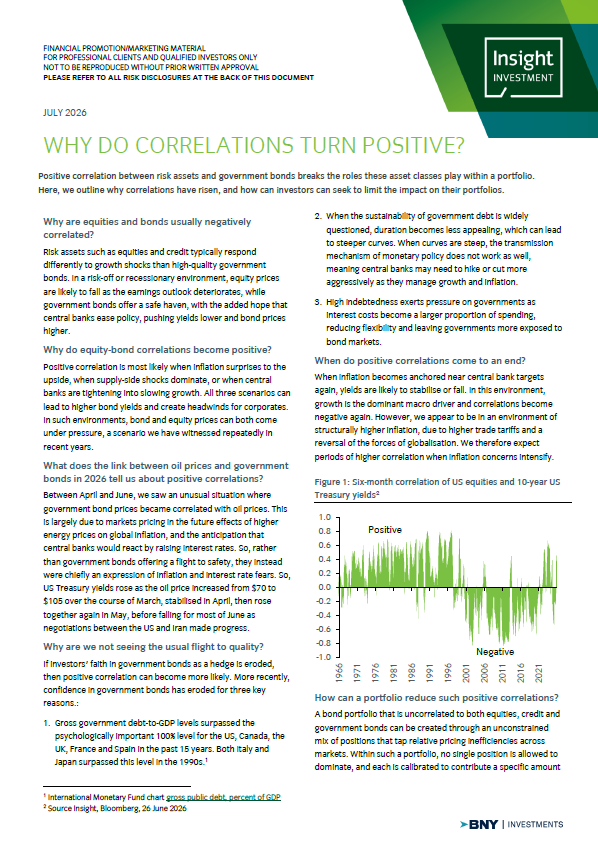

Figure 1: Six-month correlation of US equities and 10-year US Treasury yields2

What does the link between oil prices and government bonds in 2026 tell us about positive correlations?

Between April and June, we saw an unusual situation where government bond prices became correlated with oil prices. This is largely due to markets pricing in the future effects of higher energy prices on global inflation, and the anticipation that central banks would react by raising interest rates. So, rather than government bonds offering a flight to safety, they instead were chiefly an expression of inflation and interest rate fears. So, US Treasury yields rose as the oil price increased from $70 to $105 over the course of March, stabilised in April, then rose together again in May, before falling for most of June as negotiations between the US and Iran made progress.

Why are we not seeing the usual flight to quality?

If investors' faith in government bonds as a hedge is eroded, then positive correlation can become more likely. More recently, confidence in government bonds has eroded for three key reasons.:

- Gross government debt-to-GDP levels surpassed the psychologically important 100% level for the US, Canada, the UK, France and Spain in the past 15 years. Both Italy and Japan surpassed this level in the 1990s1.

- When the sustainability of government debt is widely questioned, duration becomes less appealing, which can lead to steeper curves. When curves are steep, the transmission mechanism of monetary policy does not work as well, meaning central banks may need to hike or cut more aggressively as they manage growth and inflation.

- High indebtedness exerts pressure on governments as interest costs become a larger proportion of spending, reducing flexibility and leaving governments more exposed to bond markets.

When do positive correlations come to an end?

When inflation becomes anchored near central bank targets again, yields are likely to stabilise or fall. In this environment, growth is the dominant macro driver and correlations become negative again. However, we appear to be in an environment of structurally higher inflation, due to higher trade tariffs and a reversal of the forces of globalisation. We therefore expect periods of higher correlation when inflation concerns intensify.

How can a portfolio reduce such positive correlations?

A bond portfolio that is uncorrelated to both equities, credit and government bonds can be created through an unconstrained mix of positions that tap relative pricing inefficiencies across markets. Within such a portfolio, no single position is allowed to dominate, and each is calibrated to contribute a specific amount of risk. Such absolute return bond portfolios can also be tailored to limit correlation with traditional risk assets and to take long or short positions.

Conclusion

Heightened geopolitical risk and more frequent market shocks are increasing the likelihood that bonds and risk assets move together. To preserve the defensive role of bonds, we believe investors should broaden the scope for managers to build portfolios that are less reliant on traditional sources of return and more resilient overall.

Most read

Fixed income

July 2026

Monthly fixed income review and outlook

Global macro, Fixed income

October 2023

Yield-curve inversion – an unreliable recession signal?

Global macro, Economics

May 2023

Why central banks may struggle to solve the inflation puzzle

Economics, Global macro

June 2025