United States

United States

|

Headline CPI came in better than the market expected. Consumer prices were unchanged in October, following a 0.4% and 0.6% increase in September and August, respectively. On a year-on-year basis, CPI eased from 3.7% in September to 3.2%.

Core CPI (albeit still more stubborn) also came in better-than-expected, at 0.2% month-on-month and decelerated from 4.1% to 4.0% year-on-year – the slowest pace since September 2021, with softer inflation prints across the number of categories. In our view, this makes it more likely that the Fed's hiking cycle is over.

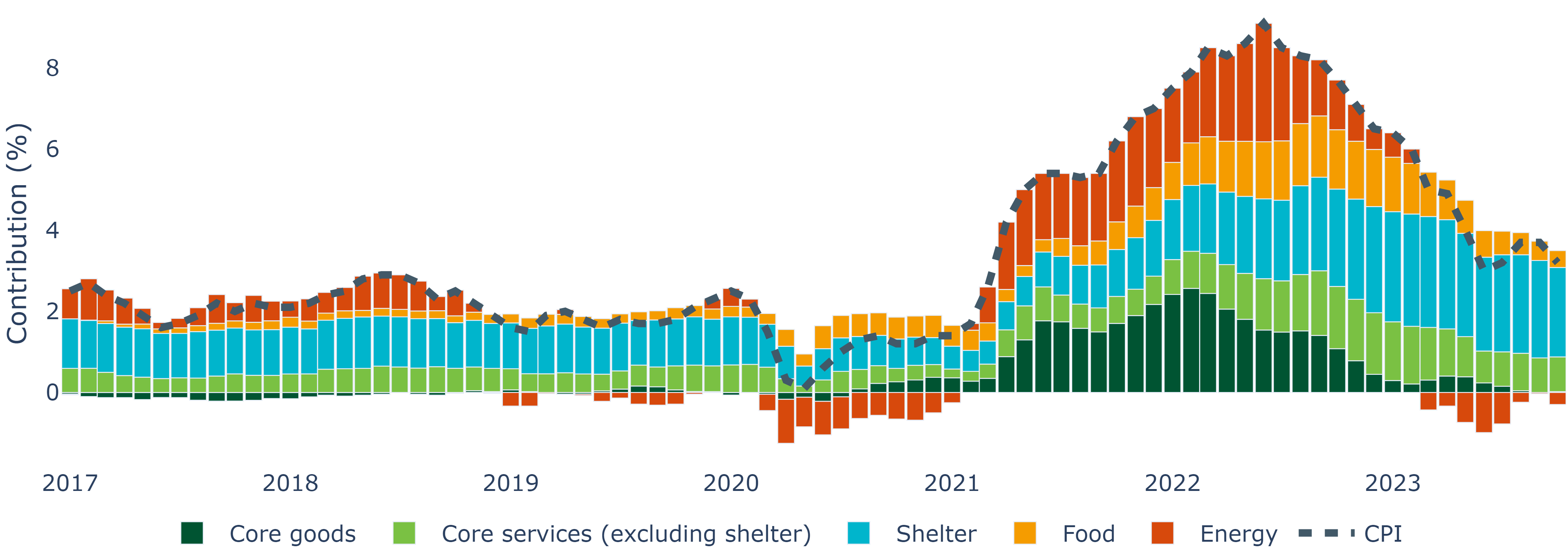

Negative energy CPI helps push headline CPI down

The energy price index fell 2.5% in October, amid retreating fears that the Israel-Hamas conflict will disrupt global supply. Prices also fell in categories such as durable and nondurable goods, private transportation and education and communication.

Figure 1: Energy CPI goes negative again

Source: Bureau of Labor Statistics, Insight, November 2023

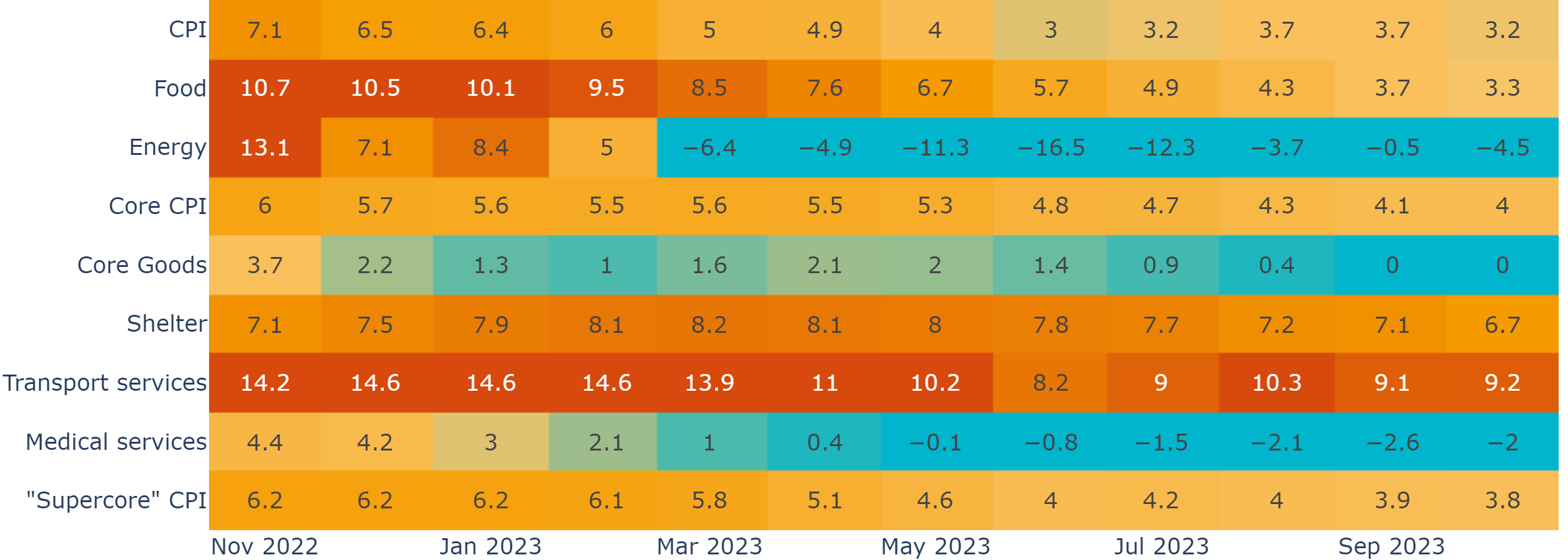

We also saw some progress in “stickier” categories, such as shelter (following a surprisingly strong print last month) (Figure 2). On the other hand, food prices accelerated to 0.3% in October, following a string of 0.1-0.2% monthly gains in the prior five months. Elsewhere, medical prices generally rose modestly, partly due to a periodic calculation reset in medical insurance.

Figure 2: Disinflation continues to be evident across most categories

Source: Bureau of Labor Statistics, Insight, November 2023

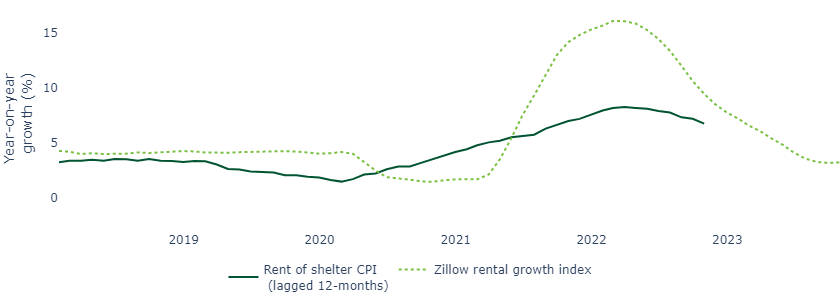

Shelter disinflation is particularly encouraging and we think there is more to come

We have watched shelter CPI closely because it is the largest and “stickiest” component of the index. Rental prices change relatively slowly (as they typically get locked in for a year) and their index calculation is largely based on surveys that the Bureau of Labor Statistics refreshes every six months.

Encouragingly, shelter is now running at its slowest level since September 2022 on a year-on-year basis. We believe it will continue moderating over the next several months. Studies show that, directionally, shelter CPI lags private rental indices (such as one maintained by Zillow) by up to a year (Figure 3).

Figure 3: We think there is more disinflation to come in the shelter component

Source: Bureau of Labor Statistics, Zillow, Insight, Bloomberg, November 2023

Inflation will remain a hot topic in 2024

Although this was an encouraging data release, we continue to expect that the path to the Fed’s target of 2% inflation will be a bumpy one.

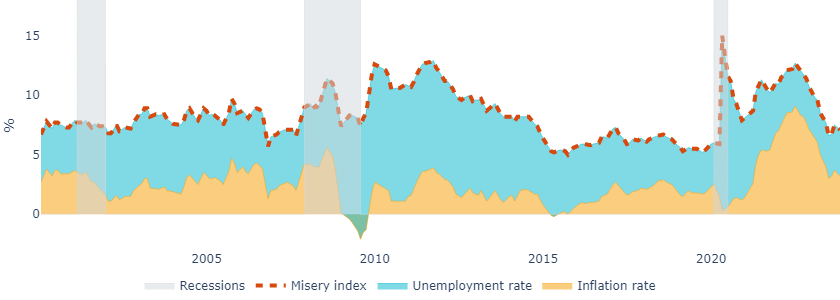

Above-target inflation will also likely play into the discourse surrounding the upcoming presidential campaign given inflation’s importance with voters. The “misery” index (which is a sum of the annual inflation rate and the unemployment rate) aims to capture how voters are doing economically. For now, it may paint an encouraging picture for the incumbent administration, but the impact up until the election remains uncertain (Figure 4).

Figure 4: Falling inflation has depressed the “Misery Index”

Source: Bureau of Labor Statistics, NBER, Insight, November 2023

We are, however, more confident about what it means for the Fed in the near-term. The slowdown in shelter (in particular) makes it even more likely to us that the hiking cycle is over. Even if the central bank maintains a hawkish messaging stance, we suspect it may also be more confident about achieving its prized “soft landing”.