United Kingdom

United Kingdom

- Trustees and sponsors have an unprecedented opportunity to secure wider benefits for their members and corporates.

- This is possible due to the improved funding status of many defined benefit (DB) pension schemes and the evolution of sophisticated risk-management techniques, enabling ongoing investment without compromising the security of members’ retirement income.

- An insurance buy-out is therefore not the only option – conducting a buy-out could mean unnecessarily giving up a significant asset.

- From a member’s perspective, a buy-out may only be appropriate if the insurer’s credit rating is at least equivalent to the combined support of the scheme surplus and its corporate sponsor.

An opportunity for significant benefits for all

DB schemes have an unprecedented opportunity to provide pensions to their members while also creating the potential to deliver enhanced benefits to the people who helped grow them over preceding decades – members and sponsors – and society more broadly.

Specifically, they have the scope to potentially:

- offer enhanced benefits for members who have worked for many years to build up their pension savings, and offset the erosion of the real value of their benefits by high inflation;

- reimburse some of the capital that sponsors have historically contributed to enhance the security of pension benefits;

- improve the intergenerational equity and security of pension provision through support for defined contribution (DC) schemes of their sponsor; and

- provide finance to support economic growth.

Pension schemes can grow their surplus with high certainty

These benefits are possible because of the improved funding status of many schemes and the evolution of sophisticated risk-management techniques.

- Many DB pension schemes have now shifted into a surplus, meaning they have more assets than needed to meet projected future liability payments, even under a prudent set of assumptions for the future. In part due to a dramatic rise in gilt yields in 2022, most schemes are now in surplus.

- Investment and risk-management techniques have evolved considerably over the last 10 years, meaning many schemes can now, through investments that generate contractually defined cashflows, achieve, secure and grow their surpluses – without compromising the security of members’ future retirement income.

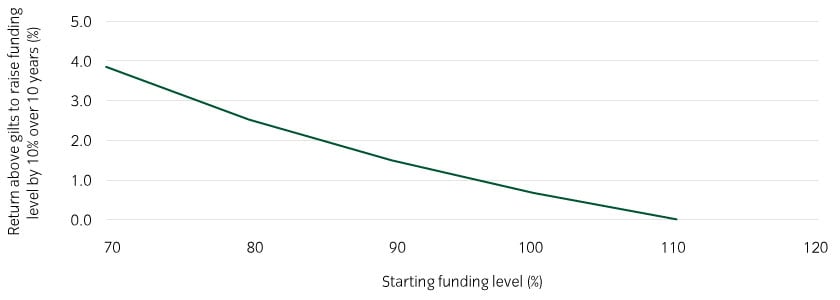

This becomes clear when considering the investment returns a pension scheme needs to achieve to improve its funding level. A pension scheme in surplus can follow a very conservative investment strategy and still achieve significant growth (see Figure 1).

This means that pension schemes can now be considered an asset, rather than a burden.

Figure 1: Well-funded pension schemes only need very low returns over gilts to boost their funding level

For illustrative purposes only. Source: Insight as at 31 May 2023

To offer an example, a pension scheme could invest today in high-quality corporate bonds to achieve a contractually defined return of gilts plus 1% to 1.5% per annum. For a fully funded1 £1bn scheme with a 15-year duration, this level of excess return would equate to an additional asset valued at c.£150m to c.£225m after 10 years. The question is whether the ‘value’ of such future surpluses should be given away2.

Buy-out may not be the best option for all pension schemes

Insurance buy-outs remain attractive in some circumstances, but we believe it is outdated to assume they are the best option for most schemes.

Historically, with many pension schemes underfunded, it was natural for many trustees and sponsors to perceive their pension scheme as a burden. The long downward trend in yields increased liabilities – and when pension schemes are underfunded there is the risk that sponsor default, or the inability of asset growth to match liabilities, leaves a scheme unable to pay out its members benefits in full. Many sponsors have agreed material contributions to close funding gaps, only to find themselves being asked for additional contributions a few years later.

In this context, a buy-out may have appeared attractive. However, as we outline above, the situation has changed. Pension schemes are in a much stronger position today. The decision to conduct a buy-out is equivalent to a decision to give away the ability to generate additional surpluses that could be used to improve benefits for members, enhance sponsor finances, and support positive societal change. This could be equivalent to handing over an asset worth hundreds of millions, or in some cases even billions, of pounds. These could even be worth a significant proportion of the total value of the corporate sponsor.

We also note that there is growing scrutiny of the risks that may be introduced through conducting a buy-out.3 From a member’s perspective, setting aside the possibility of improved benefits, to proceed with a buy-out trustees should be comfortable that the credit quality of a pension scheme surplus combined with the backing of its corporate sponsor is inferior to the credit quality of the insurer.

Running on a pension scheme is a credible alternative – supported by The Pensions Regulator

In our experience, misconceptions often hold back trustees and sponsors from considering running on a pension scheme. These include concerns over investment risk, the potential to trigger future sponsor contributions, and legal issues involved in the sharing in the benefits of surplus. However, we believe these fears are often unfounded.

- From an investment perspective, as we outline above, with a sufficiently well-funded pension scheme, techniques already exist to enable further surpluses to be secured in a contractual fashion without the need for additional dependency on the sponsor.

- From an actuarial perspective, for schemes that have already secured the required future contractual returns, dynamic discount rates can take this into account – meaning market movements need not trigger unnecessary contributions from the sponsor.

- From a legal perspective, mechanisms already exist for most schemes and sponsors to share in the benefits of a surplus above a prudent level of funding (as outlined above).

Therefore, if there is a desire to retain the ability to generate additional surplus in a secure fashion, and the ongoing benefits that accrue from it, then investment, actuarial and legal considerations are unlikely to be roadblocks to achieving this.

The Pensions Regulator has explicitly acknowledged that running on a pension scheme may be a better option: “You may consider that running on the pension scheme is a better option for your members, as it offers them potential to benefit from future surpluses. Your employer may also have concerns over trapped surpluses or prefer an ongoing arrangement allocating some surplus to fund scheme expenses, future accruals or, depending on the legal structure of your scheme, to benefit members in a DC section.”4

Given the above, we would challenge readers to consider what other motivational factors may be stopping UK DB pension schemes from realising the potential benefits available from c.£1.5 trillion of capital – such as discretionary increases in benefits for members in the next cost-of-living crisis, lessening the financial burden on sponsors while providing an effective DC arrangement for employees, and providing finance that can help support wider society in the future.

Next steps for your pension scheme

If you would like to discuss the implications for your pension scheme, please contact us. |